Choosing a Health Insurance Plan for International Students

Coming to study in the United States is an exciting opportunity for international students from around the world. As you make preparations for your academic studies, an important consideration is choosing a health insurance plan that meets your needs while living in the U.S.

Selecting the right health insurance can provide you with peace of mind, ensuring you have access to medical care if you get sick or injured. This article explains what to look for when comparing student health insurance plans, key factors to consider when choosing coverage, and provides an overview of some basics about U.S. health insurance.

What to consider when purchasing health insurance in the U.S.

International students will need to have health insurance when coming to the United States. In order to maintain their international student visa status, the student must have a student accident and health insurance plan, according to the Student and Visitor Exchange Program (SEVP). Some schools may require a student to use a specific insurance provider, or a plan that meets their specifications. Other schools may let their international families purchase their own coverage. Check your school’s policies to see if they have any specific requirements.

Here are some key factors to keep in mind as you review health insurance options:

- Coverage of pre-existing conditions – A pre-existing condition is an illness or injury that you had before enrolling in a new health plan. Many student health plans exclude pre-existing conditions or have a waiting period before they will cover treatment for these conditions. If you have an ongoing health issue, you’ll want to look for a plan that covers pre-existing conditions with no waiting period.

- Emergency services – Make sure the plan covers emergency room visits and hospitalization inside and outside your school area in case you have a medical emergency when traveling.

- Doctor visits – You’ll want to understand how much you pay for going to see a doctor. Many plans require a copay, which is a fixed amount you pay per visit.

- Prescription drugs – Check whether your regular prescription medications are covered and how much you will pay. You don’t want to be surprised with extremely high medication costs.

- Medical evacuation – If you have a serious injury or illness and need to be transported home for treatment, medical evacuation can be extremely expensive. Choose a plan that includes this coverage.

- COVID-19 coverage – The COVID-19 pandemic is ongoing, so make sure your plan covers testing and treatment for COVID-19.

- Network of providers – You want to have doctors and hospitals nearby that accept your insurance so you can easily get care. Avoid plans with very small networks.

- Customer service – Pick a plan with a helpful customer service team that can answer your questions in your native language. You want support getting care.

Health Plans: The Basics

When researching U.S. health insurance plans, you may come across unfamiliar terms like deductible or copayment. Here’s a breakdown of what these terms mean:

- Deductible: A fixed amount you have to pay before the insurance company will start to pay for medical expenses. Many student plans have a $100 to $500 deductible per injury or illness.

- Copayment: A fixed amount (for example $20-$40) you will pay each time you receive a specific medical service. Copayments typically apply to doctor’s office visits, emergency room visits, and prescription medications.

- Coinsurance: After you’ve paid your deductible, this refers to the portion of medical expenses you will pay. It’s shown as a percentage. For example, you pay 20% while the plan covers 80%.

- Out-of-pocket maximum: This puts a cap on your costs for the year. Once you reach this amount in deductible, copays and coinsurance, the plan covers 100%.

- Premium: The upfront cost of the plan. Make sure to understand how often you pay the premium (monthly, quarterly or annually).

Selecting a Health Plan

Plans with higher premiums tend to have lower deductibles and copays, while plans with lower premiums have higher deductibles and copays. How can you determine the right plan? Here are some key questions to consider:

- How often do you expect to see a doctor during your studies? Frequent doctor visits mean a low-deductible plan with copays makes sense.

- Do you take regular prescription medications? Make sure your medications are covered and choose a plan with reasonable drug copays.

- Do you play competitive sports with a high injury risk? An accident-prone student athlete may want a plan with a lower deductible and coinsurance.

- What medical costs could you afford to pay out-of-pocket if you had an unexpected illness or accident? Choose a deductible and out-of-pocket maximum within your budget.

Many student health plans offer tiered options with differing deductibles, copays and premium costs. For example:

- High premium option: $0 deductible, low copays

- Moderate premium option: $250 deductible, moderate copays

- Basic premium option: $500 deductible, higher copays

Review the details to pick the option that best fits your medical needs and budget. Also make sure you understand the plan’s out-of-pocket maximum costs.

Plan Limitations and Exclusions

All health insurance plans have coverage limitations and exclusions. These are medical services that are either limited in some way or not covered at all. It’s important to read the plan details to be aware of the limitations and exclusions so you know what is not included in your coverage.

Here are some common limitations and exclusions to look out for:

- Pre-existing conditions – Many student health plans exclude pre-existing conditions, have a 6-12 month waiting period before covering them, or limit how much they will pay for continuing care for a pre-existing condition. Check this if you have an ongoing health condition.

- Prescription drugs – Most plans only cover generic drugs or require you to pay extra for brand name prescriptions. Some expensive specialty medications may not be covered. Make sure your medications are included.

- Routine vision and dental care – These services are often excluded or you may need to purchase add-on coverage.

- Immunizations – Routine immunizations required by your school may not be covered.

- Sports injuries – Injuries related to intercollegiate, intramural, or club sports may have limited or no coverage.

- Mental health services – The number of mental health counseling visits may be capped at a low number like 5-20 per year.

- Pregnancy – Prenatal care, delivery and newborn care are usually excluded from student health plans.

- Pre-authorization – Your plan may require pre-authorization and referral from your student health center before you can see an outside doctor or specialist.

Carefully reviewing the plan’s fine print ensures you understand what medical care is covered as well as any limitations that may impact you.

Get matched to the best program for you

Whether you are looking to attend a community college, vocational program or a top U.S. university, we can help you find the right school and program based on your interests, academics and budget. Our personalized counseling service will:

- Help you identify the right degree and field of study based on your career goals, strengths and interests.

- Provide expert guidance on which schools are the best fit for you and your budget.

- Walk you through the entire application process step-by-step from researching programs to submitting your applications.

- Offer tips to improve your application essays and help you find scholarships to make U.S. education affordable.

- Advise you on student visa requirements and guide you through obtaining your visa.

- Get you set up with housing, airport pickup, orientation and everything you need to succeed when you arrive at your new school!

We have over a decade of experience helping international students from more than 115 countries find success in the U.S. higher education system. Our personalized approach and expertise provides you with the support you need to achieve your dreams of studying in America!

Why Choose WorldTrips Atlas Travel Insurance

WorldTrips Atlas Travel Insurance is a good option for travelers to the USA who want comprehensive coverage at an affordable price. The plan is easy to buy online and includes a number of benefits, such as 24/7 emergency assistance and travel delay coverage.

If you’re planning a trip to the USA, I recommend getting a quote for WorldTrips Atlas Travel Insurance today as below:

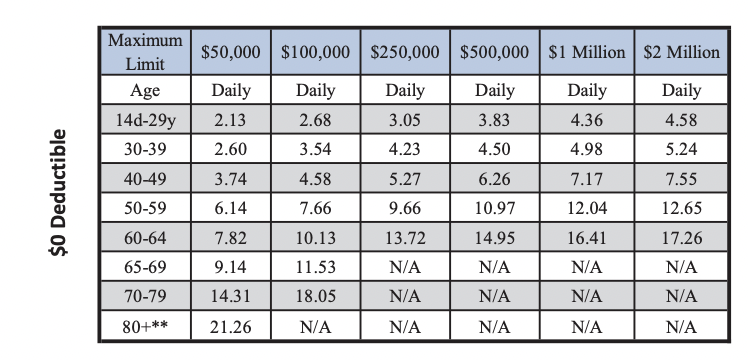

Rates

Related articles

Is Utah State a Good Place to Study?

Update to English Proficiency Scores at A-State

Is Early Decision (ED) Binding?

Study in the USA at Robert Morris University

College of Central Florida enjoys Graduate Employment Rate of 86%

Ivy League Schools – Why Called the “Ivy Leagues?

Ready to start your journey?

Leave your details — our team will tailor a free plan for you.

Get free consultation